What’s The Net Worth? Unveiling The Secrets Of Wealth In Today’s World

Let’s talk about something that’s on everyone’s mind—money! More specifically, what’s the net worth? It’s a term we hear all the time, whether it’s about celebrities, business moguls, or even ourselves. But do you really know what it means? Spoiler alert: it’s not just about how much cash you’ve got in the bank. Net worth is a snapshot of your financial health, and it’s way more important than you might think.

Imagine this: you’re scrolling through social media, and you see someone flaunting their luxurious lifestyle. You can’t help but wonder, “What’s their net worth?” It’s natural to be curious, but understanding net worth goes beyond gossip. It’s about taking control of your own finances and building a stable future.

So, why does net worth matter? Whether you’re trying to climb the corporate ladder or just want to save up for that dream vacation, knowing your net worth is the first step toward financial freedom. Stick around, and we’ll break it down for you in a way that’s easy to digest—and maybe even fun!

Read also:Cheerleader Alison Butler Herbstreit The Ultimate Story You Need To Know

Here’s a quick roadmap to help you navigate this article:

- What Is Net Worth?

- Why Does Net Worth Matter?

- How to Calculate Your Net Worth

- Celebrities and Their Net Worth

- Average Net Worth by Age

- Tips for Increasing Your Net Worth

- Common Mistakes to Avoid

- Net Worth vs. Income

- Setting Financial Goals

- Final Thoughts

What Is Net Worth?

Alright, let’s dive into the basics. So, what exactly is net worth? Simply put, it’s the difference between what you own (assets) and what you owe (liabilities). Think of it like a financial report card—it gives you a clear picture of where you stand financially.

Here’s the formula:

Net Worth = Assets – Liabilities

Let’s break it down further. Assets include things like your savings, investments, real estate, and even your car. Liabilities, on the other hand, are your debts—things like mortgages, student loans, and credit card balances. Subtract the latter from the former, and voilà, you’ve got your net worth.

Why Understanding Net Worth Is Crucial

Knowing your net worth isn’t just for the rich and famous. It’s a tool that everyone can use to assess their financial health. Whether you’re just starting out or you’re well into your career, understanding your net worth helps you make smarter financial decisions.

Read also:Court Date Search Broward The Ultimate Guide To Finding Your Court Dates

For example, if your net worth is negative, it’s a sign that you might need to rethink your spending habits or focus on paying off debt. On the flip side, if your net worth is growing, it’s a good indicator that you’re on the right track.

Why Does Net Worth Matter?

Now, you might be wondering, “Why should I care about my net worth?” Well, here’s the deal: your net worth is a reflection of your financial habits and decisions. It’s not just about how much money you make; it’s about how well you manage it.

Think about it this way. Two people might have the same income, but their net worths could be vastly different. One person might be saving and investing, while the other is spending everything they earn. Over time, those choices add up, and your net worth is the ultimate scorecard.

Having a positive net worth also gives you peace of mind. It means you’re building wealth, not just living paycheck to paycheck. And let’s be real, who doesn’t want that?

Long-Term Benefits of a Positive Net Worth

A positive net worth can lead to all kinds of awesome things. For starters, it gives you more financial freedom. You’ll have more options when it comes to big life decisions, like buying a house, starting a business, or retiring early.

Plus, a solid net worth can help you weather unexpected storms. Whether it’s a medical emergency or a job loss, having a financial cushion can make all the difference.

How to Calculate Your Net Worth

Alright, let’s get down to business. Calculating your net worth isn’t as hard as it sounds. All you need is a pen, paper, and a little bit of honesty. Here’s a step-by-step guide:

- Make a list of all your assets. This includes your bank accounts, retirement accounts, investments, real estate, and any valuable possessions.

- Add up the total value of your assets.

- Make a list of all your liabilities. This includes your mortgage, student loans, car loans, credit card debt, and any other debts you might have.

- Add up the total value of your liabilities.

- Subtract your liabilities from your assets. The result is your net worth.

It’s important to be as accurate as possible when calculating your net worth. Don’t round up or down—be honest with yourself. After all, the goal is to get a clear picture of your financial situation.

Tools to Help You Calculate Your Net Worth

If math isn’t your strong suit, don’t worry. There are plenty of tools and apps that can help you calculate your net worth. Some popular options include Mint, Personal Capital, and YNAB (You Need a Budget). These tools not only calculate your net worth but also help you track your progress over time.

Celebrities and Their Net Worth

Let’s talk about the big dogs—the celebrities with net worths that make our jaws drop. Whether it’s tech tycoons, movie stars, or athletes, their financial success is often the stuff of legends. But how do they do it?

Take Elon Musk, for example. As of 2023, his net worth is estimated to be around $250 billion. That’s billion with a “B.” How did he get there? By founding and leading companies like Tesla, SpaceX, and Neuralink. It’s not just about having a good idea—it’s about executing it and taking risks.

Then there’s Dwayne “The Rock” Johnson. With a net worth of around $800 million, he’s one of the highest-paid actors in Hollywood. But it wasn’t always smooth sailing for The Rock. He worked hard, stayed disciplined, and built his brand over time.

What Can We Learn from Celebrities?

While most of us won’t reach billionaire status, there’s still a lot we can learn from these financial powerhouses. For starters, they prioritize investments and diversification. They don’t put all their eggs in one basket—they spread their wealth across different assets.

Another key takeaway is the importance of branding. Whether it’s through social media, endorsements, or side businesses, many celebrities have built empires that go beyond their main careers. It’s a lesson in thinking outside the box and exploring new opportunities.

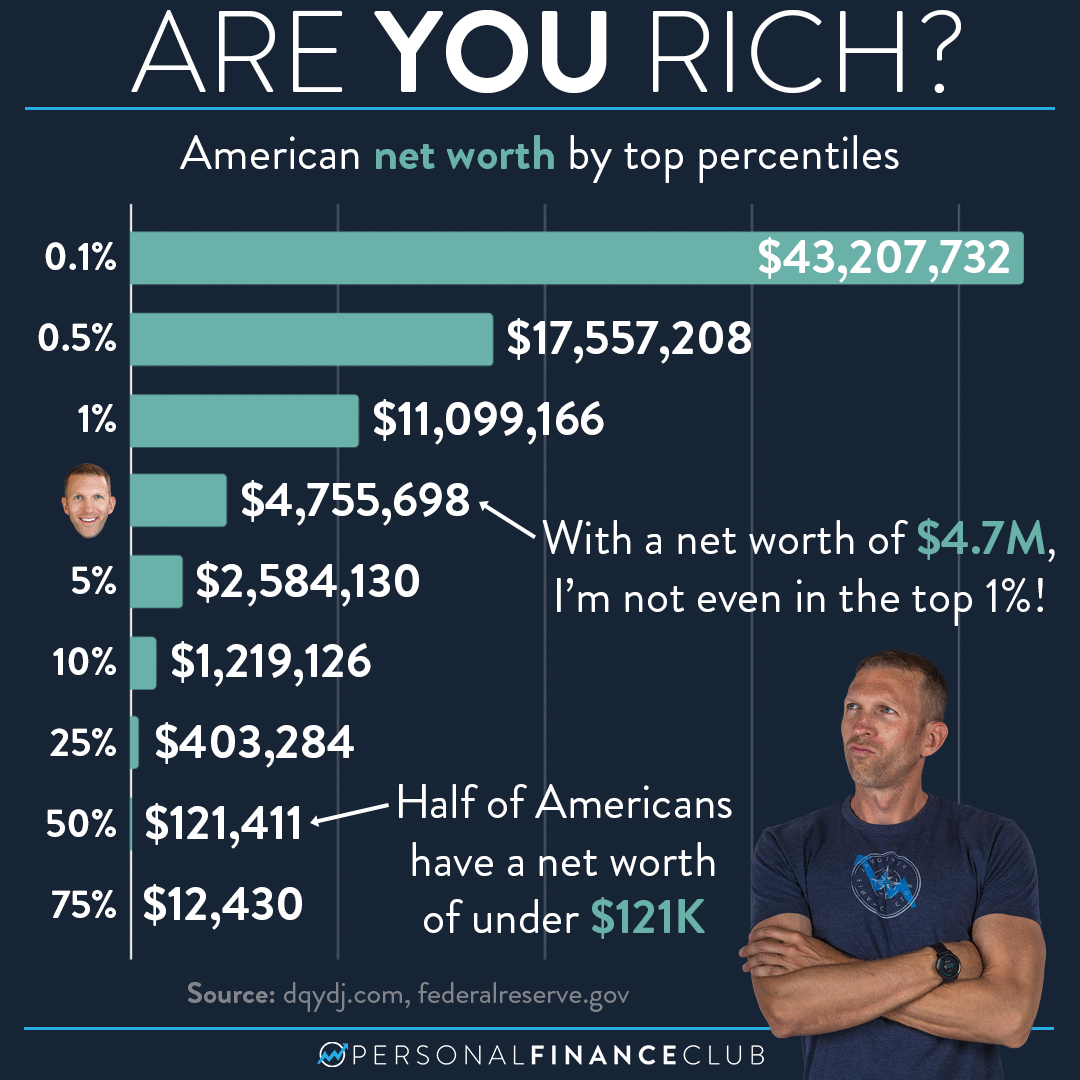

Average Net Worth by Age

So, how does your net worth stack up against others in your age group? Let’s take a look at some averages:

- Under 35: $76,200

- 35-44: $436,200

- 45-54: $833,200

- 55-64: $1,175,900

- 65 and over: $1,217,700

Keep in mind that these are averages, and they can vary widely depending on factors like location, education, and career choices. But they do give you a general idea of where you should be at different stages of life.

If your net worth is lower than the average for your age group, don’t panic. It’s never too late to start building wealth. The key is to take action and make a plan.

Why Age Matters in Net Worth

Your age plays a big role in your net worth because it affects how much time you have to save and invest. The earlier you start, the more time your money has to grow. That’s why financial experts always emphasize the power of compound interest.

For example, if you start saving $500 a month at age 25, you could have over $1 million by the time you’re 65 (assuming a 7% annual return). But if you wait until you’re 35 to start saving, you’ll need to save about $1,000 a month to reach the same goal. Time is truly money when it comes to net worth.

Tips for Increasing Your Net Worth

Alright, let’s talk solutions. If you’re ready to boost your net worth, here are some actionable tips:

- Live below your means. This one might sound obvious, but it’s crucial. Spend less than you earn, and save the difference.

- Pay off high-interest debt. Credit card debt can be a major drag on your net worth. Prioritize paying it off as quickly as possible.

- Invest in your future. Whether it’s stocks, real estate, or retirement accounts, investing is one of the best ways to grow your wealth over time.

- Build multiple income streams. Don’t rely on just one source of income. Explore side gigs, passive income opportunities, or even starting your own business.

- Stay educated. The financial world is constantly changing, so it’s important to stay informed. Read books, attend seminars, and follow trusted financial advisors.

Remember, building wealth is a marathon, not a sprint. It takes time, patience, and discipline. But with the right mindset and strategies, you can achieve financial independence.

Common Pitfalls to Avoid

While we’re on the topic of increasing net worth, let’s talk about some common mistakes to avoid:

- Lifestyle inflation. As your income grows, it’s tempting to upgrade your lifestyle. Resist the urge to spend more and focus on saving instead.

- Ignoring retirement savings. Many people put off saving for retirement, thinking they have plenty of time. The truth is, the earlier you start, the better.

- Taking on unnecessary debt. Not all debt is bad, but some types, like credit card debt, can be toxic. Be mindful of how much debt you’re taking on and why.

Net Worth vs. Income

Now, let’s clear up a common misconception: net worth and income are not the same thing. Income is the money you earn from your job or other sources, while net worth is the difference between your assets and liabilities.

Why does this distinction matter? Because you can have a high income but a low net worth if you’re not managing your money wisely. On the flip side, someone with a modest income can have a solid net worth if they’re saving and investing consistently.

So, don’t get caught up in comparing your income to others. Focus on building your net worth, and you’ll be on the path to financial success.

Setting Financial Goals

Finally, let’s talk about setting financial goals. Having clear goals is essential if you want to improve your net worth. Here’s how to get started:

- Define your short-term and long-term goals. Short-term goals might include paying off debt or building an emergency fund, while long-term goals could be buying a house or retiring early.

- Make your goals specific and measurable. Instead of saying “I want to save more money,” say “I want to save $10,000 in the next 12 months.”

- Break your goals into smaller steps. Big goals can feel overwhelming, so break them down into manageable chunks. For example, if you want to save $10,000 in a year, aim to save $833 per month.

- Track your progress. Regularly review your goals and adjust them as needed. Celebrate your successes along the way!

Remember, financial goals are personal. What works

{kind=link}